How Credit Score Affects Approval for Auto Loans

You’ve finally had it with your old vehicle. You’ve spent months looking around, shopping for the best deals, and figuring out what kind of car you’d like to have, and you’ve finally found the new car that you would like to call your own. The only problem now is obtaining the finances necessary to make the purchase. Most likely, you are looking for a lender. Shopping for auto loans can be a frustrating and confusing process. Obviously you would like to get the lowest interest rate possible, and there are many different companies trying to get your business, all with different plans. So the question is: what is the best plan I can get, and how high should I settle?

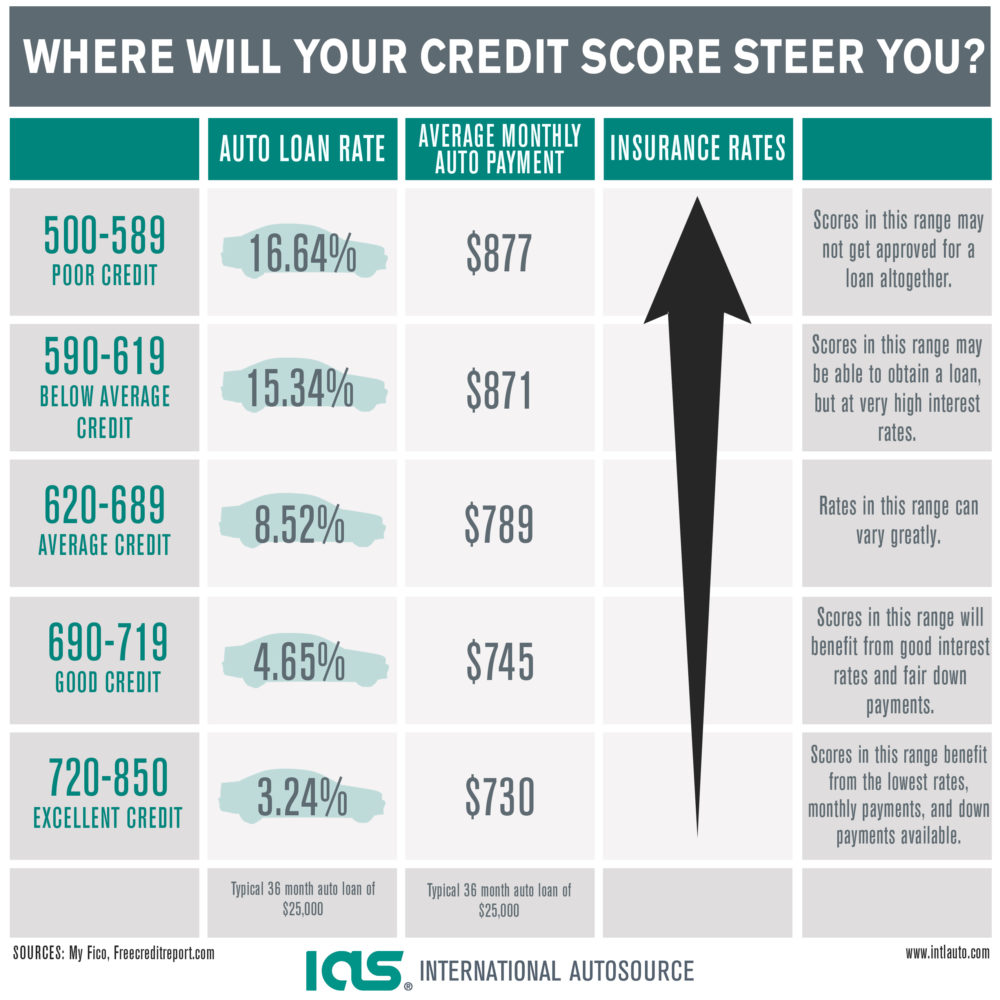

One of the most important factors to understand when applying for auto loans is your credit score. Every time you apply for any type of credit, that business will make an inquiry with a credit agency. You will be rated at a number between 300 and 850, with 300 representing the highest risk and 850 representing the lowest risk. The vast majority of people are rated somewhere between 600 and 800, and factors that may affect your credit ranking include number of credit channels, number of inquiries made recently, timeliness of bill payments, and any negative reports or collections filed.

It is good to keep in mind that if you are shopping for auto loans, student loans, or home mortgages, any inquiries made within the past 30 days will be counted as one inquiry. Contrast this with inquiries made by credit card companies, which will all appear on your statement. The point is, shopping around for auto loans will not negatively affect your eligibility, so you might as well keep searching for the best deal possible.

When it comes to what sort of interest you’ll be able to get, your score will be looked at. Generally, someone who is rated higher than 680 will be eligible for low interest, while those above 700 will receive the best deals. As long as your score is higher than 600, you will most likely not be considered a high risk, and will probably be able to get a decent deal.

Once you understand how your score relates to your ability to obtain a loan, how do you know what your rank is? You might be surprised to know that different agencies will give you a slightly different rating. This mostly depends on what type of credit or loan you are looking to get, so keep this in mind when shopping. To get a general idea of how you stand, you can file a personal inquiry and find out your own credit score.

All in all, searching for auto loans should not be a very stressful process. Armed with the knowledge of how you are sized up by lenders, you should be able to navigate the system and be on your way to getting the ride you deserve.